Medicare and Private Insurance Health Care Prices Diverge Substantially in 2022

August 24, 2022

From the spring of 2021 through June of this year, the U.S. has been in a period of high and rising economywide price inflation. Pressures such as labor scarcities, global energy interruptions, and supply chain disruptions have made everything from consumer goods to business services more expensive. Yet, in our ongoing series of Health Sector Economic Indicators (HSEI) briefs, we have been detailing data that find, quite surprisingly, overall inflation for the health care sector—as measured by the aggregate Health Care Price Index (HCPI)—has remained in a very tight and modest range, rarely exceeding three percent year-over-year growth or falling beneath two percent growth. In our monthly briefs, we have explored how factors such as the time it takes for new contracts and reimbursement rates to take effect and recent policy changes restraining public health care costs have kept overall health care inflation well below economywide rates. As these factors continue to play out, the recently-released July price data are revealing what may be a key inflection point in Medicare and private insurance prices for health care services.

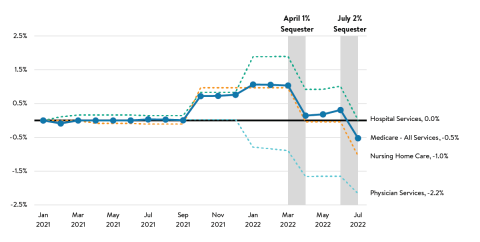

In July, the prices paid for many types of health care from these two major payer types diverged substantially. Medicare prices fell by nearly a full percentage point, putting overall Medicare services prices below the levels seen back in January 2021 (Exhibit 1). These declining Medicare prices are due to two major factors: very low or no increases in the statutory reimbursement rates for hospital care and physician services in the calendar year 2022 and the re-institution of the mandated sequestration cuts for Medicare provider payments in April and July of this year. These sequestration cuts, which had been postponed for many years since they were updated in 2011, are having a meaningful impact as seen in the chart below. The impact of the two sequestration cuts can be seen clearly in the data, pulling down Medicare prices between March and April and then between June and July across all three major settings of care as first a 1% and then a 2% cut were put in place. Due to the fact that physician services received relatively smaller baseline increases in new Medicare rates for 2022, the sequestration cuts have pulled those price levels the lowest, down by 2.2% since January 2021. Medicare price changes for nursing homes care fall in between hospitals and physician services, down by 1.0% since January 2021.

Medicare Health Care Price Growth and Major Components, Cumulative since January 2021

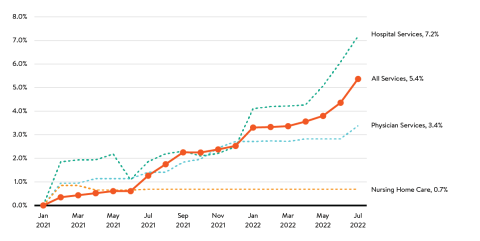

At the same time Medicare prices are falling, the prices for similar types of care paid by private insurance increased substantially in July, up a full percentage point from the previous month and 5.4% higher than the price levels in January 2021 (Exhibit 2). We believe many of these increases are occurring as new contracts or updated rates are slowly taking effect, and further expect there may be a noticeable discrete jump in private prices beginning in 2023, as recent comments from providers and insurers are stating 2023 negotiations are generally favoring providers. We can see in the data that it appears hospitals are experiencing much higher private price growth than other components (up 7.2% since January 2021) and faster recent growth, with price levels increasing by nearly a full percentage point in each of the past three months. Physician services are the next fastest growing component, while nursing home private prices have barely moved since the beginning of 2021. Faster increases in hospital prices may indicate stronger negotiating positions for those providers, particularly given ongoing consolidation in the industry over the past ten years.

Private Insurance Health Care Price Growth and Major Components, Cumulative since January 2021

When looking at the HCPI in aggregate, these two diverging trends have been cancelling out, leading to overall moderate growth in health care prices. Yet, these detailed, by-payer data indicate that significant trends in health care prices are occurring underneath, with the long-expected increases in private prices beginning to follow overall economywide inflation trends. All else equal, these price increases in care paid by private insurance will further exacerbate an already wide gap between public and private prices. This is especially true for hospital care, where the disparity between Medicare and private prices diverged by a whopping 7.2 percentage points in the last eighteen months. The most important factors driving the trends going forward for private prices will be the extent to which overall economywide inflation slows and who has the balance of power in insurer/provider contract negotiations. For public prices, government policy decisions will continue to be most important influencer of their growth. We expect to follow all these factors and the overall impact of the diverging data on overall health sector inflation in our ongoing series of HSEI briefs through the rest of the year and into 2023.